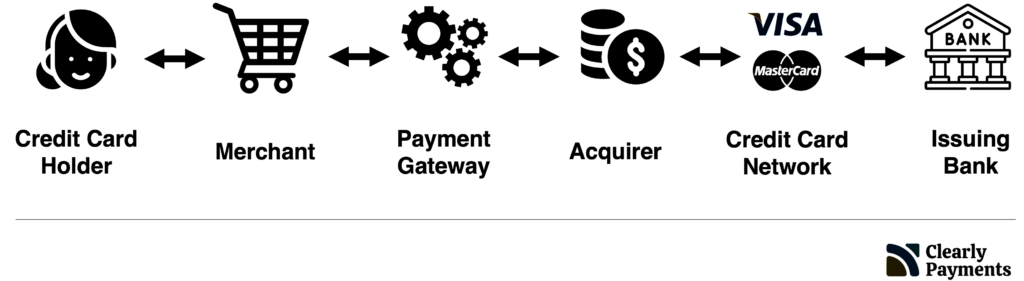

Credit card networks refer to the financial systems that enable consumers to make purchases using their credit cards. They act as intermediaries between merchants, credit card issuing banks, and cardholders. Credit card networks provide the infrastructure and technology necessary to process credit card payments. They play a critical role in enabling the widespread adoption of credit cards as a convenient and secure form of payment.

The major credit card networks include Visa, Mastercard, American Express, and Discover. These networks process billions of transactions every year, generating billions of dollars in revenue. They also offer additional services, such as fraud protection and dispute resolution, to consumers and merchants.